MARKETS IN A NUTSHELL — FOR MARCH 2026

Investors began March assuming that the rich world had slain the inflation beast and interest rates would continue to trend lower. By the Ides they were confronting a rather older problem: the consequences of war in the Middle East on energy prices, inflation and interest rates. The Israeli-American attack on Iran, and the effective closure of the Strait of Hormuz to oil traffic, triggered a classic energy supply shock. Brent crude surged 63% in March. Equities and bonds fell globally, with Europe among the worst hit.

What is confounding markets is not only the rise in energy prices, but the lack of an obvious way back. Share markets occasionally rallied on hints of diplomacy, but commodity markets are less willing to suspend disbelief. They are trading the physical problems of damaged infrastructure, impaired shipping, scarce insurance and the slow mechanics of restarting production, transport and refining. Even an early ceasefire would not restore normality quickly. Strategic energy reserve releases have bought some time, but they do not create supply. And supply matters most for net importers of oil, refined products and gas, particularly in emerging Asia outside of China, where fuel buffers are thinner.

The macroeconomic backdrop offers little comfort. America started March with its labour market already softening. February’s loss of 92,000 jobs was the worst non-recession data print in nearly two decades. And Europe looks more exposed still. It has scarcely recovered from the last energy crisis before being hit by another — this time with weaker growth, high public debt and less fiscal room to shield consumers as generously as it did in 2022.

Central banks are again thrust into the awkward position of confronting inflation expectations. Australia raised interest rates for the second time this year. In America, markets that once expected rate cuts are currently betting that rates will stay flat for the rest of the year. The OECD now forecasts American inflation to reach 4.2% this year — the worst among the G7 nations.

Markets responded to the oil shock in an unusually unhelpful way. Bonds fell because higher energy prices fuel expectations of tighter monetary policy. Gold — normally a haven — fell as investors sold what they could to raise cash, and as higher real yields dulled its appeal. Chinese government bonds were, however, a rare exception. China’s lower inflation, different energy mix and deeper domestic pool of buyers made it look insulated, by comparison. Elsewhere, some oil importers were already selling reserves and, in places, US Treasuries to steady their currencies and pay larger energy bills. In that sense, the shock is also tightening global liquidity.

FOORD FUND PERFORMANCE

Foord’s funds have been conservatively positioned for some time, avoiding outsized weightings to the frothiest areas of the market. While we could not have foreseen the joint attack on Iran, we had prepared portfolios against the worst effects of any external shock. This took the form of diversification, judicial asset allocation, preference for safer equities and bonds instead of those trading near all-time highs, holding non-correlated investments, and the use of derivative hedging at the margin.

The result was that the Foord funds performed near the top of their respective peer groups in March. Given the market rout, this meant our funds typically declined much less than benchmarks and peers. Protecting investors against loss is, after all, a hallmark of the Foord investment philosophy.

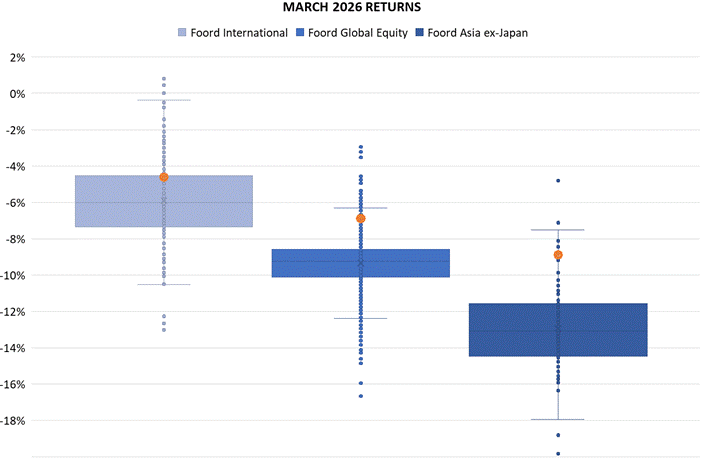

The following box-and-whisker chart shows the range of returns for the peer group sectors of key investment strategies for the month of March 2026. Each box contains the middle 50% of fund returns, while each whisker encloses the top and bottom quartiles. Outliers are shown as single dots, with the Foord funds shown as orange circles. Every Foord fund shown outperformed at least 75% of other funds with similar investment strategies.

Our Foord Asia ex-Japan Fund declined almost 9% but outperformed 90% of funds with a similar investment objective. A focus here on better quality companies at better valuations paid off. Ditto the Foord Global Equity Fund. The Foord International Fund was perhaps not quite as resilient as might have been expected. The derivative hedges paid out nicely in the month, but the fund was brought lower by its precious metals investments — with gold failing as a hedge this month as noted above.

THE PATH FORWARD

Looking forward, share markets are likely to trade on hope, while commodity markets will trade on logistics. Rising transport prices will squeeze corporate margins as well as consumer wallets — a double whammy to profits. Whether this may prompt recession is not yet clear. What is clear, though, is that politics is once more shaping inflation, interest rates, currencies and capital flows concurrently. In such a setting, portfolios built for several plausible outcomes, with liquidity preserved and balance maintained, are likely to prove more useful than those built around a single guess about how quickly the world will calm down.

Share this on:

Insights

07 Apr 2026

MARKETS IN A NUTSHELL — FOR MARCH 2026

Investors began March assuming that the rich world had slain the inflation beast and interest rates would continue to trend lower. By the Ides they were confronting a rather older problem: the consequences of war in…

10 Mar 2026

That's just nuts — Foord's latest children's book

Investing isn’t always about numbers, graphs, markets and economics. At Foord it’s also about acorns, squirrels, woodpeckers, tortoises and now monkeys. Author and Foord communications manager, CHRISTINA CASTLE,…